Month two: the leaderboard flipped

Last month I published the first month of forward-return data for 20+ screening strategies. Momentum and quality led, classic value lagged, and every strategy finished positive on a strong up-market. The caveat was front and centre: one cohort each, one month, so none of it proved a durable edge. The only way to tell skill from a good tape is to keep measuring.

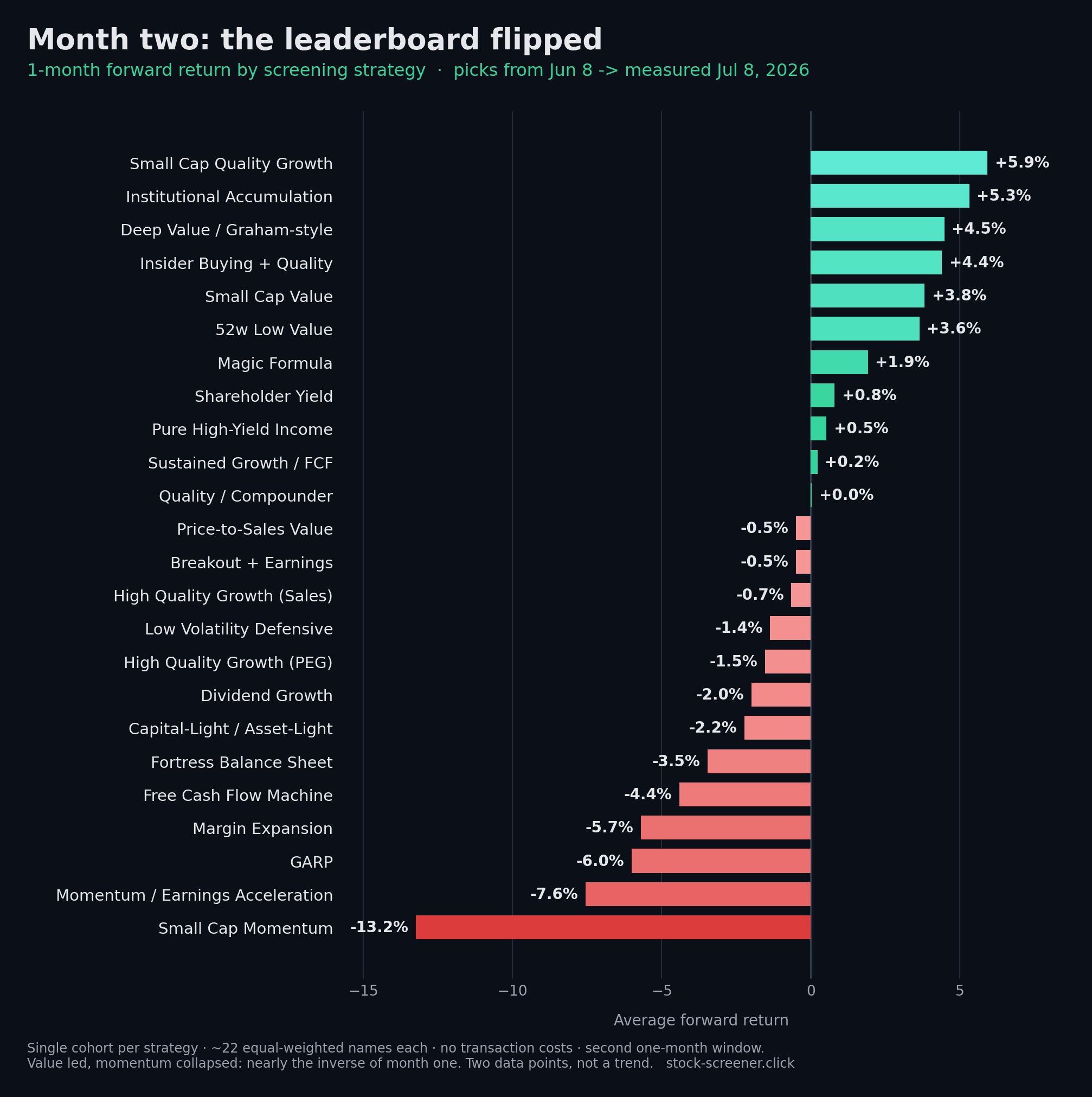

Month two is in, and it did something the first post can only have hoped for as a teaching moment: it nearly turned the whole board upside down.

How this was measured

Same method as last time. For each strategy I take the cohort of tickers it picked on a given past date, enter at the first available close after that date, and measure the average percent return to the latest close. These numbers come from picks made on June 8, 2026, measured to July 8, 2026, a fresh one-month window that does not overlap last month's. Each cohort is about 22 equal-weighted names (a couple are smaller). No transaction costs.

The leaderboard, two months side by side

The "last month" column is the real May 2 → June 1 result from the first post, so you can watch each strategy move. A few screeners are new to the board this month and have no prior figure.

| # | Screening strategy | 1-mo (June) | Last month |

|---|---|---|---|

| 1 | Small Cap Quality Growth | +5.9% | n/a |

| 2 | Institutional Accumulation | +5.3% | n/a |

| 3 | Deep Value / Graham-style | +4.5% | +0.9% |

| 4 | Insider Buying + Quality | +4.4% | +8.5% |

| 5 | Small Cap Value | +3.8% | +2.1% |

| 6 | 52w Low Value | +3.6% | +3.0% |

| 7 | Magic Formula | +1.9% | n/a |

| 8 | Shareholder Yield | +0.8% | +5.0% |

| 9 | Pure High-Yield Income | +0.5% | n/a |

| 10 | Sustained Growth / FCF | +0.2% | +6.9% |

| 11 | Quality / Compounder | +0.0% | +13.7% |

| 12 | Price-to-Sales Value | -0.5% | n/a |

| 13 | Breakout + Earnings | -0.5% | +10.0% |

| 14 | High Quality Growth (Sales) | -0.7% | +12.8% |

| 15 | Low Volatility Defensive | -1.4% | +11.6% |

| 16 | High Quality Growth (PEG) | -1.5% | +11.3% |

| 17 | Dividend Growth | -2.0% | +4.8% |

| 18 | Capital-Light / Asset-Light | -2.2% | +12.3% |

| 19 | Fortress Balance Sheet | -3.5% | +11.8% |

| 20 | Free Cash Flow Machine | -4.4% | +9.2% |

| 21 | Margin Expansion | -5.7% | +11.4% |

| 22 | GARP | -6.0% | +16.5% |

| 23 | Momentum / Earnings Acceleration | -7.6% | +18.1% |

| 24 | Small Cap Momentum | -13.2% | +12.4% |

What stood out

- The board didn't shuffle, it inverted. May's three best cohorts were Momentum / Earnings Acceleration (+18.1%), GARP (+16.5%) and Small Cap Momentum (+12.4%). In June those same three finished 23rd, 22nd and dead last, at -7.6%, -6.0% and -13.2%. The single best strategy of May was one of the worst of June.

- Value finally had its month. Deep Value / Graham-style, which was last on the May board at +0.9%, came third at +4.5%. Small Cap Value and 52-week-low Value climbed into the top six too. The classic value cohort was the only group that stayed reliably in the green.

- Risk came off. Where May had every strategy positive on a rising tide, more than half the board was negative in June, and the highest-beta, highest-growth names took the worst of it. Even "Low Volatility Defensive" slipped to -1.4%, so this was less a clean flight to safety than a broad rotation out of momentum and growth into value.

What's next

Two months in, the case for the multi-cohort view is obvious: instead of judging each strategy on its single latest pick date, average forward returns across every past pick date, so one lucky or unlucky entry stops swinging the whole ranking. That is the next piece. I'm also still digging into consensus picks, the tickers several independent strategies flag at once, to see whether agreement across screeners holds up better than any single one did here.

Want the data behind this?

Daily picks, consensus signals, and cohort-based performance, all as a simple JSON API, with a free tier.

Get it on RapidAPI →